IN ADDITION TO PROPERTY TAX FRAUD THERE WAS PUBLIC GRAFT AND CORRUPTION INVOLVING THE ABUSE OF PUBLIC OFFICE FOR PRIVATE GAIN IN THE FORM OF CRONYISM, THE USE OF UNDUE INFLUENCE IN COERCION OF FELLOW CITY OFFICIALS & SELF DEALING IN REAL ESTATE

SMOKING GUN # 1 (see both images below)

ABOVE—subject property owned by Theokas & Richner—and its original assessed value before perps’ private, tax assessment appeal meeting on March 24, 2011 with the 3 members of Grosse Pointe Park’s Board of Review*. The assessor’s original valuation of $417,800 produced an annual property tax bill to the perps of $25,877.

*The Board of Review is a body of 3 residents of Grosse Pointe Park who are appointed by the City Council, to meet with taxpayers in March of every year, who want to appeal their property’s assessed value in order to lower their annual property tax bill.

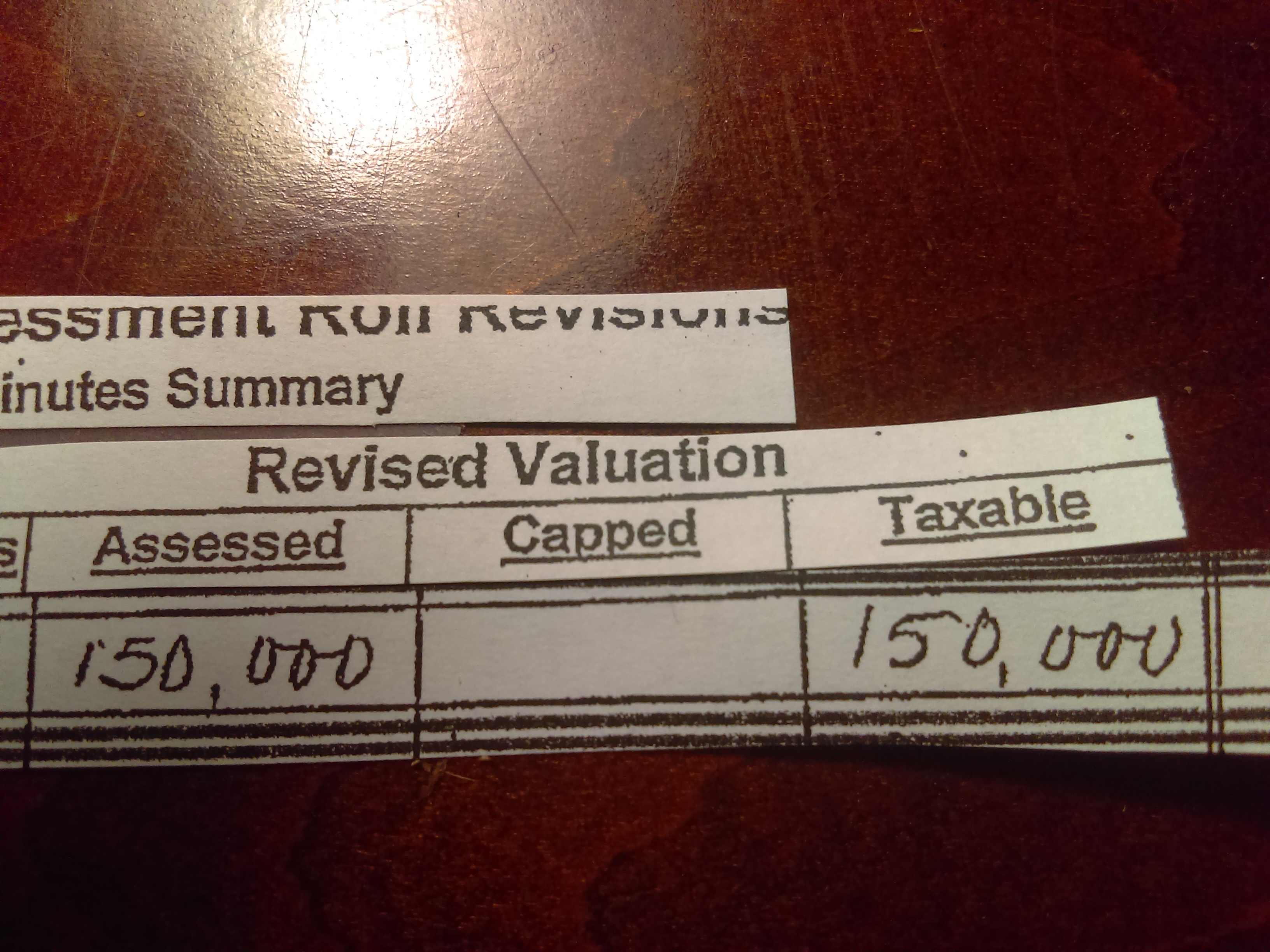

ABOVE–subject property’s revised assessed value by the Board of Review, $150,000 (a $267,800 reduction) after perps’ private, tax assessment appeal meeting with the Board of Review–resulting in revised annual property taxes of $9,285–down from $25,877 (see above).

The outcome of the private tax assessment appeal meeting referenced above–a whopping illegal property tax discount of $16,592 for 2011 (correct tax of $25,877 less the bogus revised tax of $9,285) and illegal property tax discounts going forward, escalating in an amount exceeding the illegal 2011 discount amount, in every year through 2020 and beyond in perpetuity for former Grosse Pointe Park Mayor Gregory Theokas & former Grosse Pointe Park City Council Member Andrew Richner.

In their ten years of owning the property the cumulative illegal property tax discounts total $175,000. They still own the property so this graft will continue in to the future as long as they own the property.

How did the amount of graft reach that level? In that meeting one can see by the images above that the bogus revised taxable assessed value was capped at $150,000 (revised downward from $417,800), on which the calculation of the revised 2011 property taxes was based–and on which the calculation of subsequent annual property taxes was based going forward, with minimal annual adjustments for inflation.

And by the way–lest you think there was a good reason for the Board of Review to discount the the assessed value of the property in 2011, the very next year, in 2012, the city assessor hiked the assessed value of the property back up to the former level of valuation that existed before the one time illegal discount accommodation granted to Theokas & Richner –while the property taxes remained going forward based on the bogus discounted valuation granted in 2011. Does this not smack of a cover-up?

May 4, 2020

To the residents of Grosse Pointe Park:

It is incumbent upon me to bring to your attention the shocking criminal activity that took place in 2011 and the ongoing criminal activity taking place to present day, engaged in by former Grosse Pointe Park municipal government officials–former Mayor Gregory Theokas & former City Council Member Andrew Richner and others.

In a classic example of INFLUENCE PEDDLING & CRONYISM, the members of the Board of Review and the Tax Assessor were willing and instrumental participants in the criminal activity of granting an illegal 64 percent reduction, $267,800, in the amount of the subject property’s assessed value and tax assessed value currently culminating in $175,000 in lost property tax revenue over a period of ten years to the city of Grosse Pointe Park. At the twenty year mark the loss will be in excess of $350,000.

It is ongoing criminal activity because the perps are benefitting from large illegal tax discounts year after year in perpetuity as long as they own the property, as a result of the bogus artificially low, taxable assessed value illegally granted them by the Board of Review in the meeting on March 24, 2011. That artificially low taxable assessed value, effectively capped their annual property taxes going forward from 2011 with minimal annual adjustments for inflation.

Over the last several years I have brought this criminal activity to the attention of numerous government officials and agencies with the goal of spurring an investigation and prosecution. This effort sadly has failed to yield results. Therefore as a last resort I bring the matter to you, the honest, hard working, tax paying citizens of Grosse Pointe Park & Wayne County via this website. I know this activity occurred quite some time ago in 2011–but what was set in motion in 2011 has current ramifications in that it has allowed the perps, Theokas and Richner, to benefit from substantial annual illegal property tax discounts from 2011 to the present that will continue every year into the future as long as they own the property.

This is tantamount to theft amounting to significant and material losses to the city’s treasury. This should not stand!

To add insult to injury the city of Grosse Pointe Park in 2010, had under Michigan tax foreclosure law, the legal right to purchase the property, directly from Wayne County, the legal owner after its tax foreclosure, that was valued by the tax assessor at $887,000 (2 times the 2010 SEV of 443,500).

The purchase price for Grosse Pointe Park in 2010 would have been a mere sum approaching $140,000 (the amount of delinquent property taxes)–which strategically would have made sense–for Grosse Pointe Park to own a classic, recently overhauled and upgraded ($400,000 spent by former owners in improvements) 12,020 square foot vintage building, controlling a half city block on Jefferson, between Nottingham & Beaconsfield, for ongoing city planning purposes–especially for the minimal capital outlay and the 30 to 40 percent annual return it would have yielded in net rental income.

What city wouldn’t jump at the chance to buy a piece of property worth $887,000 for $140,000?

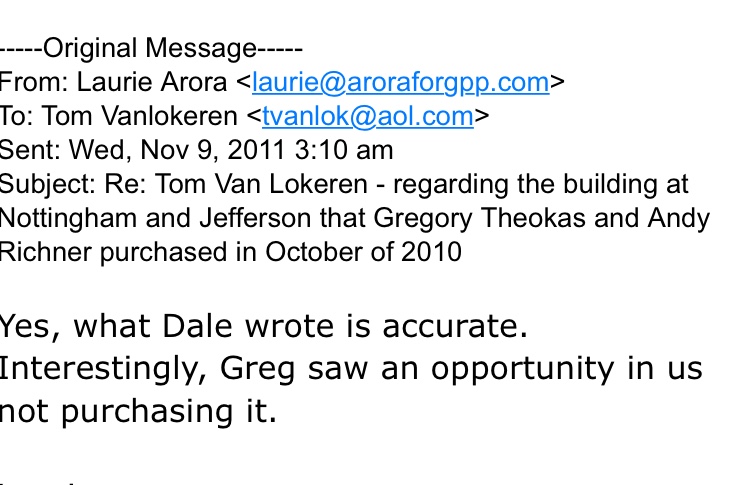

Pointe Park has engaged in many acquisitions and the development of real estate within its borders. In the summer of 2010, City Council Member and Mayor Pro Tem at the time, Gregory Theokas (perp#1), presiding over a closed door city council meeting to discuss the possible acquisition of the subject property, dissuaded the City Council from opting to have Grosse Pointe Park acquire the property. City council member at the time, Laurie Arora, was in that meeting and in a post meeting email to me in response to an inquiry, regarding that meeting, stated the following in a BOMBSHELL EMAIL:

Yes, Gregory Theokas saw an opportunity in Grosse Pointe Park “not purchasing” the property alright! Mayor Pro Tem Gregory Theokas, bought it for his own account a few months after the summer city council meeting, in the fall of 2010, at the Wayne County tax foreclosure auction, with partner Andrew Richner!

Using his influence in the affairs of city government, he steered this valuable, strategic property away from ownership by Grosse Pointe Park right in to his and Richner’s real estate portfolio.

They paid $265,400 in cash for the $887,000 property at the tax foreclosure auction and based on their purchase price of $265,400 their return on investment is estimated to be a staggering 30 to 35 percent per annum.

The return on investment would have been higher ($140,000 purchase price vs. perps’ purchase price of $265,400) and could have accrued to the city of Grosse Pointe Park if it had exercised its legal right to purchase the property. Grosse Pointe Park’s $140,000 cost of the property, would have been recovered in a matter of four years given the substantial return on investment.

The bottom line is that Theokas not only committed property tax fraud but using his Mayor Pro Tem position, unethically and unduly influenced his fellow city council members in a city council meeting, to pass up an extraordinary real estate opportunity for the city.

He and Richner then used inside information about the property, only known to city officials, to favor themselves in being the top bidder at the property tax foreclosure auction, allowing them to reap windfall returns on their ill gotten property investment, year after year, that could have accrued to the city of Grosse Pointe Park.

Some of the laws violated by the perps and city officials:

1) The well accepted and universally applied statutory law, Section 211.27 (1) of THE GENERAL PROPERTY TAX ACT of Michigan, was violated by the Board of Review and the perps and is explained in detail below further down the page.

2) The perps and the Board of Review violated and disregarded the official guidance and policy provided by The Michigan State Tax Commission in their comprehensive guide for Boards of Review. On page 18 of that guide it states that the practice by a Board of Review, of setting an Assessed Value at the sale price of a property, is illegal in Michigan. It also states that “a Board of Review does NOT have the authority to change an assessment solely on the sales price.” This is called following sales. The manual further states on that page that “the practice of following sales is a serious violation of the law. The practice of following sales results in assessments that are not uniform.”

In not following the compulsory rules, laid out in the guide for all Michigan Boards of Review, promulgated by the Michigan State Tax Commission, one can see how egregious and illegal was the nature of the Board’s granting of a 64 percent discount to the perps, amounting to $267,800 on the assessed value of a property.

Looked at another way, the Board of Review took a property whose true cash value was originally determined by the Assessor to be $835,600 in 2011 (2 times the SEV of $417,800) and revised its true cash value down to $300,000 (2 times the revised SEV of $150,000) an obscene true cash value discount of $535,600 (2 times the $267,800 assessed value discount).

Full excerpts from the Michigan Tax Commission guide for Boards of Review are located further down the page.

3) Public corruption and breach of the public trust involving the abuse and misuse of a government office for private gain That abuse and misuse took the form of cronyism and the use of undue influence to coerce other government officials’ decisions–to wit, the three members of the Grosse Pointe Board and the members of the Grosse Pointe Park city council.

The private gain derived from the abuse of office has three components 1) the illegal property tax discounts 2) the loss of equity in a property that should have been acquired by Grosse Pointe Park and 3) the 40 percent annual investment return on the acquired property.

The cumulative illegal property tax discounts (growing every year) up to this point in time amount to approximately $175,000. Grosse Pointe Park’s opportunity cost in not having acquired the property has two components–the lost equity in excess of $700,000 (Assessed value of property in 2010 of $887,000 less the $140,000 it would have required from Grosse Pointe Park to purchase the property) and $450,000 (9 years times the estimated annual net income from the property of approximately $50,000).

Add those three components up–$175,000, $700,000 and $450,000 and you arrive at the amount that Grosse Pointe Park has been fleeced out of by Theokas & Richner…$1,325,000.

From the time I found out in 2016, about this public corruption in Grosse Pointe Park’s municipal government, I have been shouting from the rooftops to those who had the power to bring the offenders to justice. That shouting has repeatedly fallen on deaf ears. Maybe this website will cause enough civic outrage toward the crimes and the aiding and abetting of that criminality by government officials, past and present, to come to a fitting, necessary and just end.

I ask for your help in raising community awareness of this public corruption in our midst and in getting it investigated and prosecuted. Since the illegal discounts are occurring every year in perpetuity I do not believe any statute of limitations protecting the perps would apply. Thank you very much in advance for your willingness to address this situation in some way, shape or form.

If you are offended and or appalled by this deplorable corruption in your own back yard, please email some or all of the parties listed at the bottom of this page to voice your outrage and demand accountability.

At a minimum email Police Chief Poloni (PoloniS@grossepointedps.org) and demand a long overdue investigation in to these matters.

Sincerely,

Tom Van Lokeren ( contact: tvanlok@aol.com )

Public Corruption: Public corruption involves a breach of public trust and/or abuse of position by federal, state, or local officials and their private sector accomplices. Public corruption in any form is the misuse of a public or government office for private gain. Its existence is an indication that something has gone wrong in the management of the government office, whether it be federal, state, or local.

Several statutes, mostly codified in Title 18 of the United States Code, provide for federal prosecution of public corruption in the United States even if those crimes were codified in state law:

The property tax crime committed in the case being presented was a violation of:

Section 211.27 (1) of THE GENERAL PROPERTY TAX ACT of Michigan – –

which states in part:

“A sale or other disposition by this state or an agency or political subdivision of this state, of land acquired for delinquent taxes or an appraisal made in connection with the sale or other disposition or the value attributed to the property of regulated public utilities by a governmental regulatory agency for rate-making purposes is not controlling evidence of true cash value for assessment purposes.”

And a failure to adhere to formal guidance and policy provided by the Michigan State Tax Commission in their guide for Boards of Review. The following is the relevant section of the guide addressing the illegal activities engaged in by the parties:

Guidance is provided to Tax Board of Review members in the following guide issued by The Michigan State Tax Commission which can be found at the following url:

To reiterate, Theokas & Richner abused the power of their offices–Theokas (Mayor Pro Tem & City Council Member at the time) along with Richner (former city council member) in unduly influencing the 3 members of the Grosse Pointe Park Board of Review in persuading them and colluding with them to illegally shave off $267,800 of taxable assessed value on the property below which they purchased in the fall of

2010 at a Wayne county tax auction.

Subject property above

What the above aforementioned statute is saying is that it is against the law for the price paid for real estate, at a public tax auction for delinquent property taxes, to be used by the assessor or the Board of Review to determine the assessed value of a property for assessing property taxes. The reason is, the price paid is not determinative of the actual true market value of a property. Why? Generally the bidders at a tax auction have incomplete information about a property they are bidding on–thus depressing bid amounts well below the actual true market value. In this case, Theokas had inside information and knew everything about the property, via his position as Mayor Pro Tem/City Council Member. Detailed financial information about the property had been provided by the former owner to the city of Grosse Pointe Park in the spring of 2010 before the fall auction. This information allowed Theokas & Richner to outlast the other bidders, knowing that the true value of the property was close to it’s assessed true cash value of $887,000 (2 x SEV of $443,500). Their winning bid was $265,400 at the property tax foreclosure auction for the subject property, a 12,020 square foot commercial property worth, as stated before, close to $887,000 (and valued as such by the assessor before the illegal discount). The Board of Review based the true cash value of the property($300,000) on an amount close to what was paid at the tax auction ($265,400), which is illegal, depriving Grosse Pointe Park of the proper amount of tax revenue.

Can you tell me that the 12,020 square foot property pictured below, with gross rents of approximately $120,000 per year and a cash on cash return on investment for the owners of approximately 30 to 35 percent per year–that its SEV (assessed value) and its taxable assesed value was $150,000?

This is an outrage!!! And this is Public Corruption which is a felony!

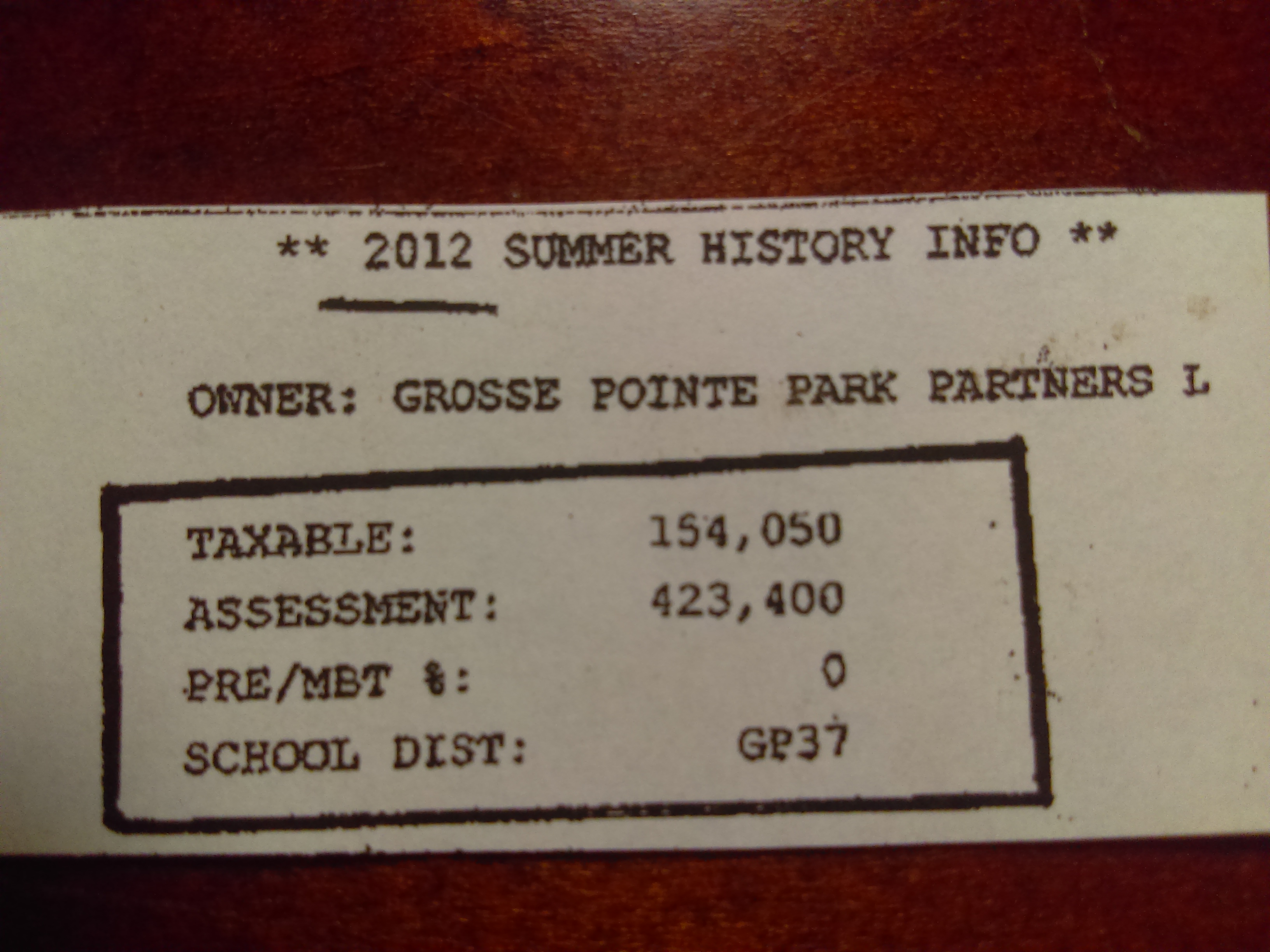

Furthermore and shockingly the $150,000 assessed value granted by the Tax Board of Review for 2011 was increased back up to its actual real assessed value of $423,400(see image below) for 2012. But the taxable assessed value, the basis on which the property taxes are computed, as opposed to its assessed value, for 2012 only increased from $150,000 to $154,050–the increase representing the capped taxable assessed value of $150,000 plus an inflation adjustment of $4,050. So it is quite apparent that the 2011 discounted taxable assessed value was a one time accommodation granted by the Board of Review to Theokas & Richner which served to cap the taxable assessed value at $150,000 in 2011 and going forward increasing by nominal annual inflation adjustments (see 2012 taxable assessment below) robbing the city of Grosse Pointe Park of substantial tax revenue year after year.

So by looking at the image below of the 2012 tax assessment, it begs the question, how is it that the Grosse Pointe Park Assessor agreed with the Board of Review’s assessed value of $150,000 in one year (2011) and the next year (2012) determined that same property’s assessed value to be $423,400. This was not a one time clerical error. In all subsequent years beyond 2012, 2013 through 2015, Grosse Pointe Park’s Assessor assessed the value (SEV) in the $400,000 to $450,000 range: 2013-$424,600, 2014-$449,200, 2015-$442,700. Assessed values beyond 2015 have not been ascertained but it is a pretty sure bet that those values stayed in the $400,000s.

All of the officials featured below, in one way or another, abdicated their responsibility to address the criminal activity that took place–criminal activity that they had been made aware of. A number of those individuals currently do not hold office now as a result of retiring, being voted out, etc.

It was a case of hear no evil, see no evil and speak no evil and PASS THE BUCK!

THIS HAD TO BE A COVER UP! IT WOULD BE HARD TO EXPLAIN IT AWAY AS COLOSSAL INCOMPETENCE AND INEPTITUDE!

Below–the chronology of OFFICIALS’ TORTUOUS EMAIL HAND OFFS OF MY Criminal Complaint, PASSING THE BUCK WITH ULTIMATELY NO ONE TAKING RESPONSIBILITY, protecting their criminal cronies!

I reported the illegal activities in 2017 to all City Council Members via email and regular usps mail. None of the City Council Members responded to me. Apparently they didn’t because it is not technically in their purview to investigate and prosecute crimes. One would think that they should have pointed me in the right direction. One also might think that it was incumbent upon them to follow up on the status of allegations of public corruption by former Grosse Pointe Park government officials robbing the city coffers. It also would seem that they had a fiduciary duty to follow up with law enforcement to see if the corruption that they had been made aware of was being addressed.

Former City Manager Dale Krajniak was also made aware of the illegal activities engaged in by former Mayor Gregory Theokas, Andrew Richner and the Board of Review through being copied on emails and other communications.

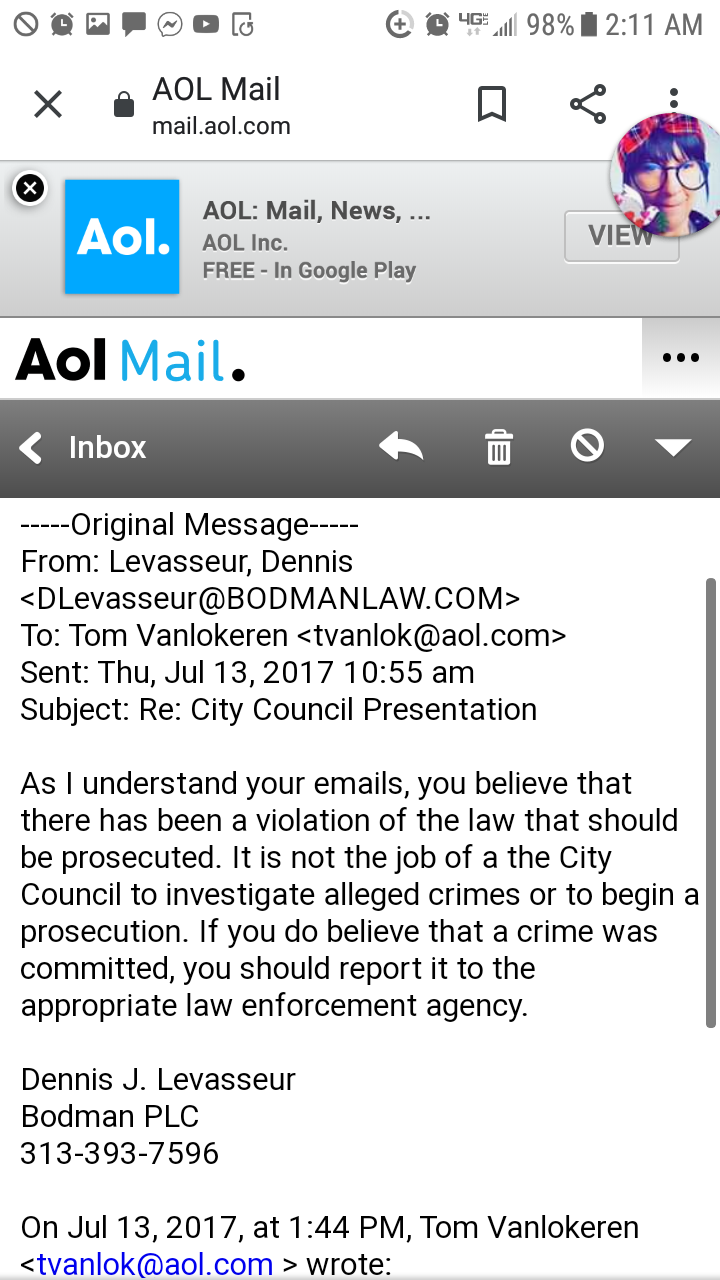

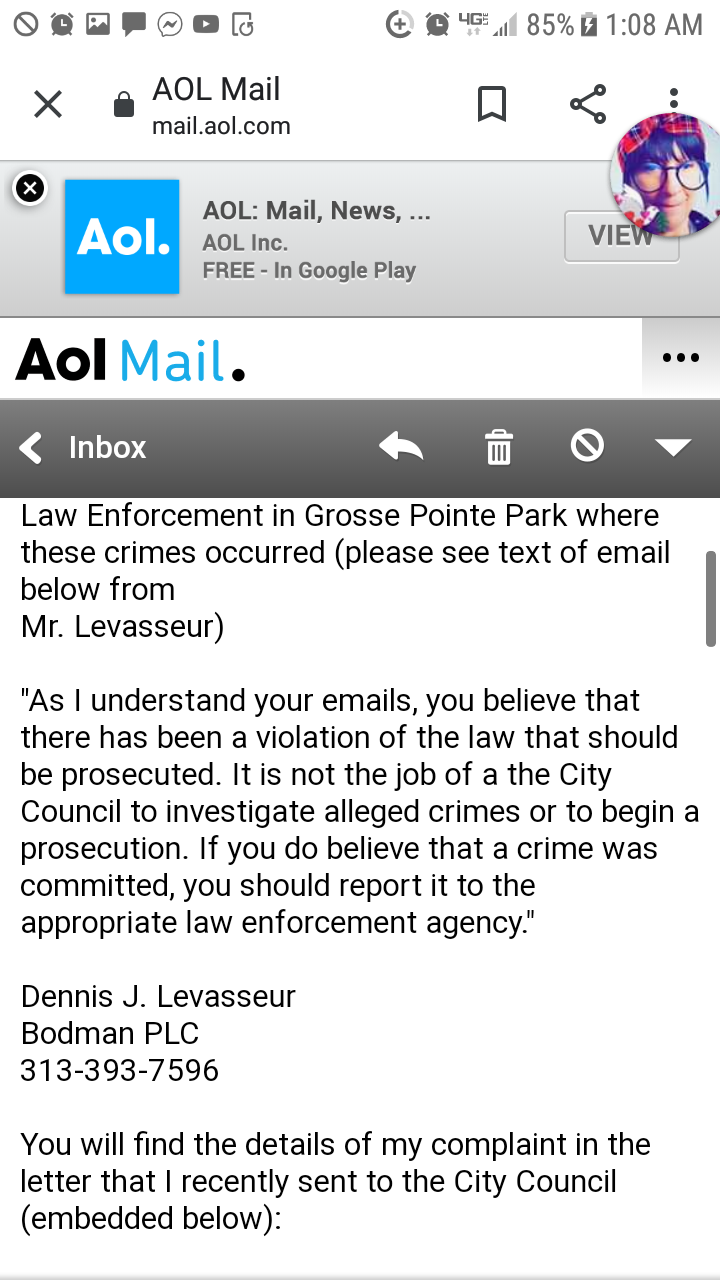

I also reported the illegal activities to the City Attorney, Dennis Levasseur–he was aware that I had contacted the members of the city council, and he expressed to me in an email “it is not the job of the City Council to investigate alleged crimes or to begin a prosecution. If you believe that a crime was committed, you should report it to the appropriate law enforcement agency” (see email below).

Notably, he failed to specify the particular law enforcement agency I should report it to. His vague and indifferent response would suggest that he really wasn’t interested in seeing this complaint progress to an investigatory stage. Otherwise he would have offered a more specific road map on how I should have proceeded. As City Attorney, it is his job to look out for the best interests of the city which would seemingly include preventing fraud and corruption and protecting the assets of the city.

Tap or click on the several email images below to enlarge.

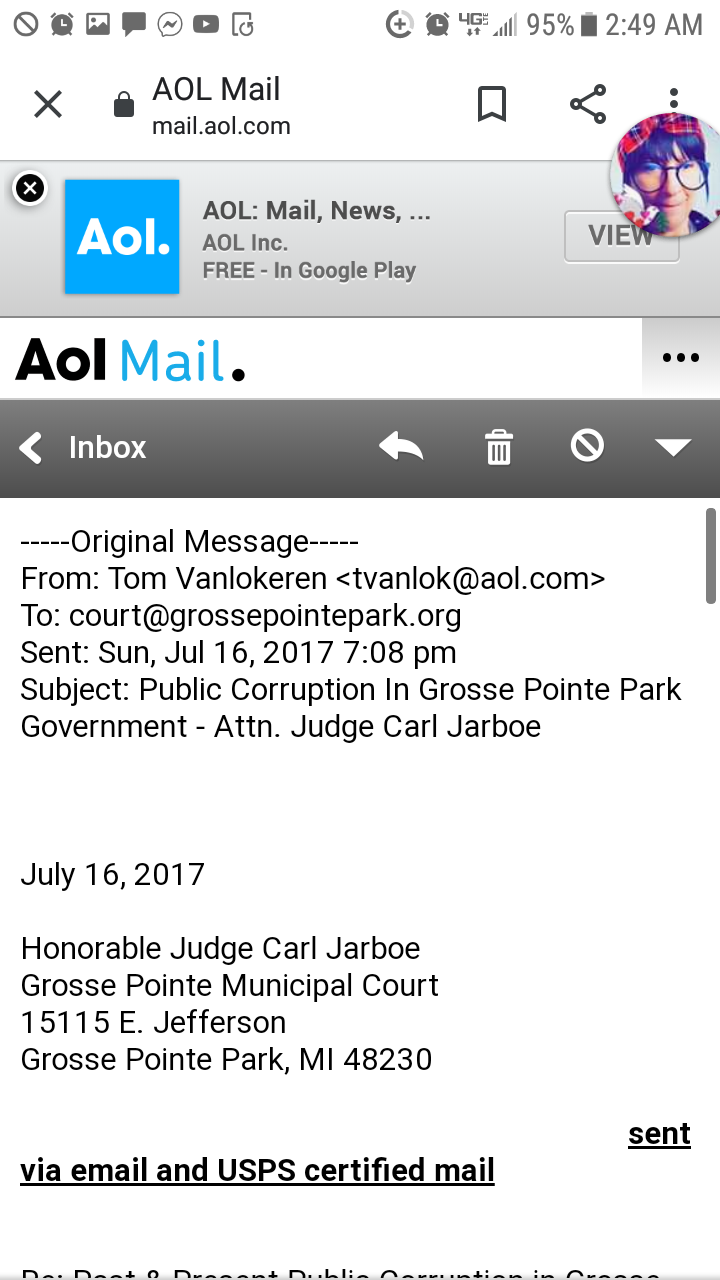

My guess, after not receiving specific guidance from the City Attorney as to exactly who to contact about illegal activities, was that the appropriate law enforcement agencies would be the court and the police so my starting point was to report the illegal activities first to Municipal Judge Jarboe (see email below).

Judge Jarboe’s office, in response to my submission of a criminal complaint, forwarded my email to current Police Chief Stephen Poloni stating in their transmittal email (see email below) that “He has a complaint and wants the matter referred to the head of the law enforcement agency here in Grosse Pointe Park. Judge Jarboe is not the party to review this. If you could do so and advise Mr. Van Lokeren as to what his rights are…” . I am copied on this email to Police Chief Poloni.

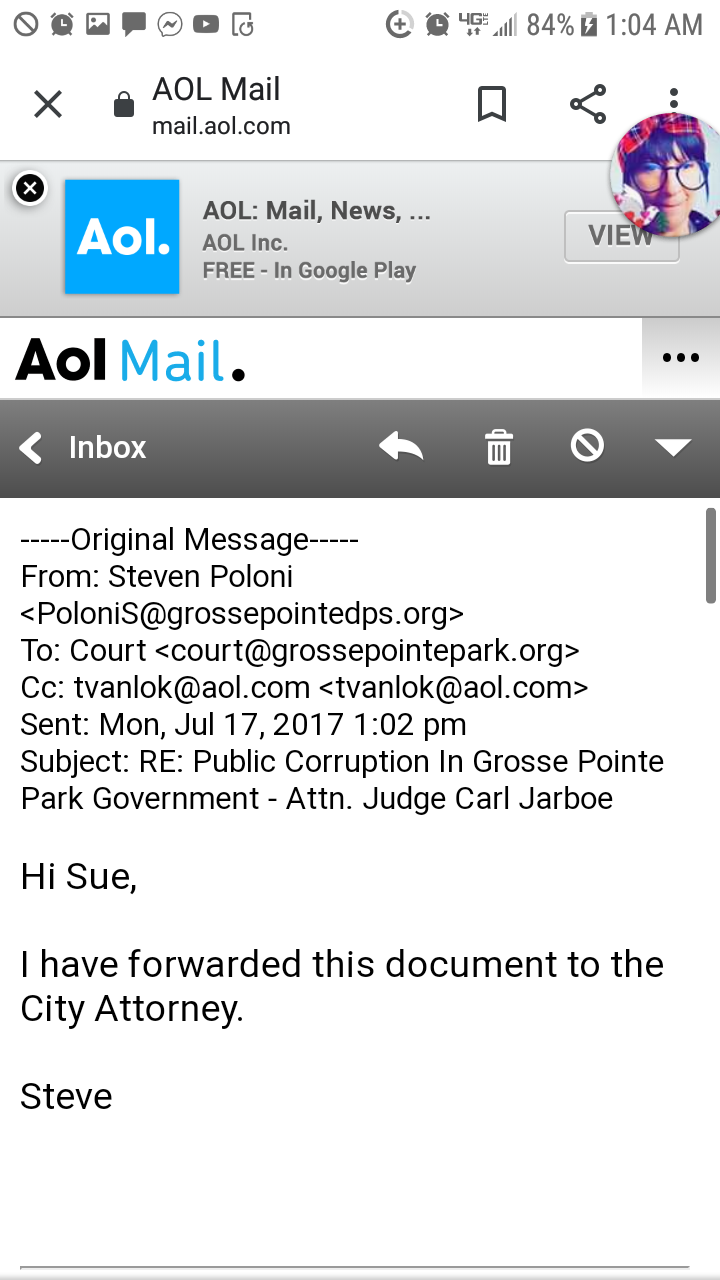

Reiterating, in the email (image above) Jarboe’s office requests that Poloni contact me “If you could do so and advise Mr. Van Lokeren as to what his rights are…”. I assumed that meant “what my rights are” with regard to filing a criminal complaint. Chief Poloni does not honor Jarboe’s request to contact me and instead forwards to the City Attorney my complaint submitted to Judge Jarboe’s office. He then emails Judge Jarboe’s office, copying me (image below), informing them that he has forwarded my complaint to City Attorney Dennis Levasseur who had just recently sent me an email informing me that I needed to contact the appropriate law enforcement agency.

So I was given the old runaround.

Judge Jarboe’s office, in an additional email to me, in response to my assertion with an example, of how a judge will sometimes initiate an investigation, conveys to me in no uncertain terms, that it’s the job of the police to investigate this crime (excerpt below):

“I have forwarded your matter to the Chief of Police, Stephen Poloni. If you have a complaint of this nature you would go through the police department. The Judge would be the one to hear whatever charges or complaint that comes from the police department and prosecutor and adjudicate the matter.”

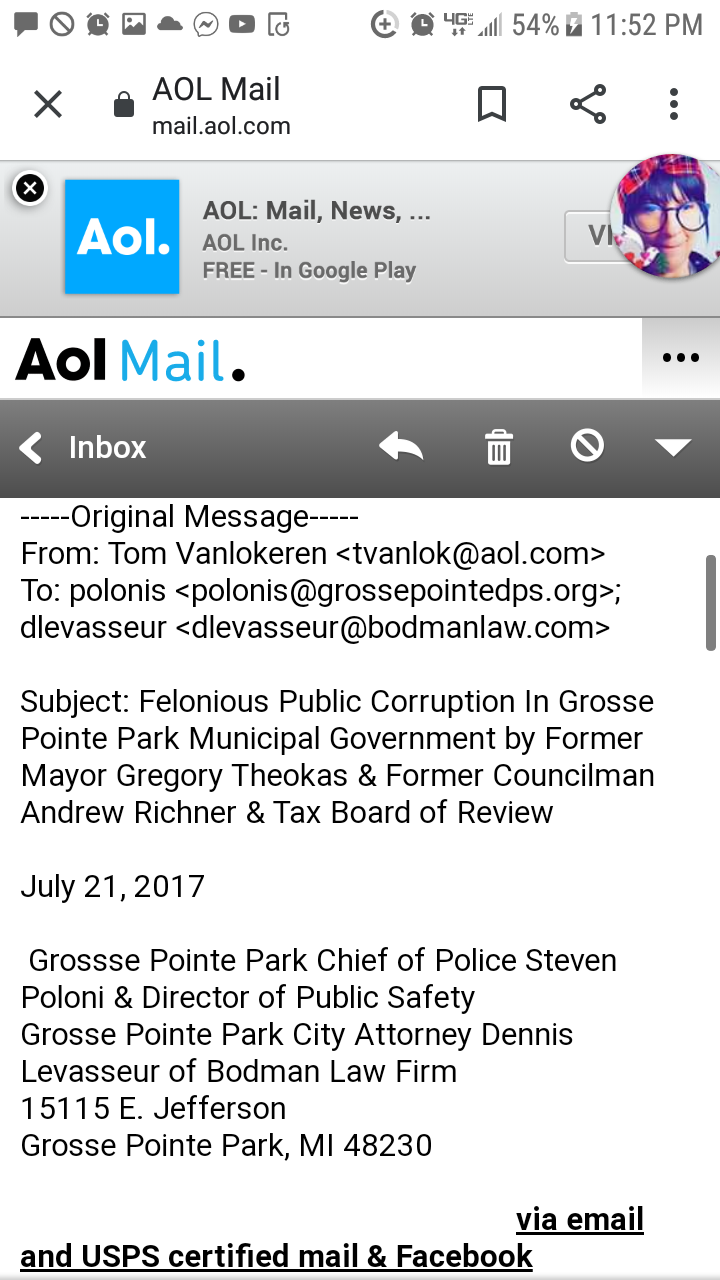

1) Since Chief Poloni failed to contact me regarding my complaint, disregarding Judge Jarboe’s instruction that he do so and 2) since Chief Poloni instead of addressing my complaint, forwarded the complaint to the City Attorney after receiving it in an email from Jarboe’s office and 3) since City Attorney Dennis Levasseur instructed me to report the crimes to the appropriate law enforcement agency, it left me with two courses of action to END THE TORTUOUS RUNAROUND 1) to at last submit my complaint in an email directly to Chief Poloni (email 1 below) and 2) to submit my complaint in one email to both Chief Poloni and City Attorney Dennis Levasseur (email 2 below).

I DID BOTH AND RECEIVED NO RESPONSE–PERIOD!. SO I GOT THE SILENT TREATMENT FROM THE TOP COP AND THE TOP LEGAL OFFICIAL IN GROSSE POINTE PARK’S MUNICIPAL GOVERNMENT.

ONE CANNOT HELP BUT ASK “WHAT IN GOD’S NAME WENT ON HERE?”

MY VOTE IS CRONYISM AND COVER-UP IN A VERY RELAXED AND CASUAL GOVERNMENT CULTURE WITH LITTLE OVERSIGHT AND THE LEGAL RIGHT TO DELIBERATE ON MATERIAL MATTERS BEHIND CLOSED DOORS (GRANTED BY AND EXEMPTION IN MICHIGAN’S SUNSHINE LAW).

email 1

email 2

ALTHOUGH WHITE COLLAR CRIME IS NOT AS OFFENSIVE AS OTHER FORMS OF CRIME IT IS NEVERTHELESS A FELONY!

TO PUT A FACE TO THE INDIVIDUALS IDENTIFIED ABOVE:

Police Chief Poloni

Grosse Pointe Park Judge Carl Jarboe

Current Grosse Pointe Park City Attorney Dennis Levasseur of Bodman Law, currently embroiled in a controversy with Grosse Pointe Park and others that has put his position as City Attorney in jeopardy.

Former City Manager Dale Krajniak, retired in 2019

Current Mayor Denner

Former City Council Member Clark

Current City Council Member Grano

Councilman Grano graduated from the University of Michigan with a BA in Political Science and Wayne State University Law School with a Juris Doctorate. He is currently an Assistant Attorney General for the State of Michigan. He is assigned to the Criminal Division and prosecutes crimes arising in the Detroit casinos, illegal gambling operations around the state, state tax crimes, and special assignments.

Former City Council Member Detwiler

Former City Council Member Chouinard

Current City Council Member Robson

Councilman Robson is currently retired from his profession and has worked as a police commander and law enforcement instructor.

Former City Council Member Arora

To reiterate — PUBLIC CORRUPTION IS A FELONY ALONG WITH MANY OF THE ASSOCIATED CRIMES THAT GO WITH THE TERRITORY! Even a theft of $1,000 by a public official is a felony. Lying on an expense report for benefit is a felony. Again your distinguished former public servants (pictured below) have stolen well over $150,000 now…increasing by $16,000-$19,000 per year!!!

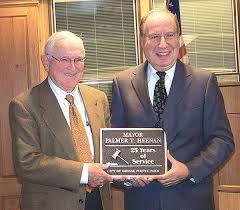

Gregory Theokas was elected to the Grosse Pointe Park City Council in 1995. He was Mayor Palmer Heenan’s right hand man as Mayor Pro Tem soon after becoming a city council member and became mayor for the time between Heenans’ retirement and the election of a new mayor. Theokas retired from office upon the election of a new mayor in 2015. Side note: There is a plaque in the Grosse Pointe Park Kercheval business district honoring the many years of service given to Grosse Pointe Park by Gregory Theokas. He resides at 824 Bishop, Grosse Pointe Park, MI 48230

Andrew Richner is a former city council member who served in the 1990s. He resides at 718 Berkshire, Grosse Pointe Park, MI 48230

Below are pictures of the perps in this ugly saga:

Picture above: Theokas to the right of Mayor Palmer Heenan

Picture above: Richner on left with unidentified individual

Theokas is a Harvard Law School Graduate with an MBA from Harvard.

Richner is a University of Michigan Law School Graduate who has held a number of prominent positions in public service over the years: Grosse Pointe Park city council member, Wayne County Commissioner and a Michigan State Representative. In recent years he was one of 8 members on The University of Michigan Board of Regents and a former Chairman of that body. I believe he is currently a law partner at the national law firm of Clark Hill.

One would think that these two pedigreed attorneys could have avoided getting their hands caught in the cookie jar! Once again hubris and arrogance trip up the privileged and powerful and the perps are caught like a deer in the head lights!

CAUGHT!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

PLEASE READ ON…THANK YOU.

$175,000 of lost property tax revenue so far……In 2 more years it will exceed $200,000…..In 10 more years it will be over $350,000……In 15 more years it will be over $400,000…….As An Honest Property Tax Paying Grosse Pointe Park Resident–WILL YOU LET THIS CORRUPTION GO UNCHALLENGED? I wonder how systemic the rot is and has been! How many other back room deals have been made over the years?

Again to reiterate, Theokas & Richner met privately with the Board of Review (a body appointed by the Mayor and City Council to meet with taxpayers who are contesting their tax assessment valuations for property tax purposes) on March 24, 2011 and obtained an obscene 64 percent discount in the taxable assessed value of a the property they purchased at a tax auction. This discount has given them massive discounts in their property taxes year after year ever since that meeting. The State of Michigan rules for Boards of Review as promulgated by the Michigan State Tax Commission (see THE LAW section further down the page) dictates that the basis upon which the Grosse Pointe Park Board of Review assessed the subject property and granted a 64 percent discount is “illegal.” The General Property Tax Act of Michigan also dictates the same (see THE LAW section further down the page).

Above: Once again the subject building –15324 East Jefferson, Grosse Pointe Park, MI 48230 (at the corner of Nottingham & Jefferson next to the gas station on Beaconsfied & Jefferson). The building is 12,020 sq. ft. with four commercial spaces on the first floor (among the tenants-Hungry Howies, Vintage Cleaners, etc.) with 9 office spaces on the second floor. The net income for the building with gross rents exceeding $120,000 per year is approximately $90,000 before taxes. There is no interest expense as they paid cash for the property. As stated earlier former Mayor Gregory Theokas & former city council member Andrew Richner received an illegal $16,577 tax discount on their property taxes in 2011 and those annual illegal discounts have continued to this day with the amounts escalating every year.

Can anybody with any credibility tell me that this property’s correct true cash value was $300,000 in 2011, with an SEV of $150,000(SEV equals one half of the true cash value) and an equal taxable assessed value ?

BELOW: Again THE SMOKING GUN!!!

Again the top image shows what the Grosse Pointe Park Assessor determined assessed values were before the corrupt meeting between three Board of Review members and real estate partners in the property–Grosse Pointe Park Mayor Pro Tem Gregory Theokas & Former Grosse Pointe Park City Council Member Andrew Richner. The bottom image shows the illegal accommodation made by the Tax Board of Review for Theokas & Richner–saving them $16,577 in property taxes in 2011 and even more than that per year in subsequent years.

Evidence of the fraud in pdf format has been uploaded to the top of a Page named Proof/Documentation . . . Click on this link. On that particular page you will see the 2010, 2011, 2012, 2013, 2014 & 2015 property tax bills and the Tax Board of Review’s notes from the meeting showing the illegal activities.

________________________________________

Top picture above: The Grosse Pointe Park Assessor’s 2012 tax bill with assessed and taxable assessed values. The Grosse Pointe Park Assessor for 2012 showed no regard for the Board of Review’s 2011 revised assessed value of $150,000 (top picture below) and put the assessed value at $423,400 but left the taxable assessed value at the revised 2011 amount of $150,000 plus the 2012 inflation adjustment of $4,050. Had the Grosse Pointe Park Assessor’s Taxable Value of $417,800 remained in place for purposes of computing the 2012 taxable value, that computation would have been $417,800 increased by a inflation factor of 2.7 percent resulting in a 2012 taxable value of $429,081 and yielding a property tax bill of $26,835. Theokas & Richner’s 2012 tax bill was $9,633. The illegal discount that the two former public officials received for 2012 was $17,202–a loss of that amount of tax revenue to the City of Grosse Pointe Park.

So in just two years the City of Grosse Pointe Park was short changed a cumulative amount of property tax revenue of $33,799 ($16,577 plus $17,202).

The calculation of lost property tax revenue through 2015 was the following for years subsequent to 2012:

2013: True and proper calculated tax of $28,018 less incorrect illegal tax billed to taxpayers–$10,020 equals lost property tax revenue of $17,999.

2014: True and proper calculated tax of $29,384 less incorrect illegal tax billed to taxpayers–$10,541 equals lost property tax revenue of $18,843.

2015: True and proper calculated tax of $30,100 less incorrect illegal tax billed to taxpayers–$10,831 equals lost property tax revenue of $19,269.

SO IN JUST 5 YEARS–2011 through 2015 the City of Grosse Pointe Park illegally lost a cumulative amount of property tax revenue of $89,890.

Extrapolate that to 20 years and you’re easily above $350,000.

________________________________________________

AGAIN–THE CENTRAL CHARACTERS IN THIS DEPLORABLE PUBLIC CORRUPTION:

Gregory Theokas – former Grosse Pointe Park Mayor/Harvard Law School Graduate. Home address: 824 Bishop, Grosse Pointe Park, MI 48230 Phone – (313) 885-2158. Owner of Mall Tooling & Engineering, Inc., 150 Grand Ave., Mt. Clemens, MI 48043.

Andrew Richner – former Grosse Pointe Park City Council member/current law partner at firm of Clark Hill/ former Michigan State Representative/former Chairman of the University of Michigan Board of Regents/ former Member of University of Michigan Board of Regents. University of Michigan Law School Graduate. Home address: 718 Berkshire, Grosse Pointe Park, MI 48230.

At a minimum please send an email to:

Police Chief of GP Park – Steven Poloni PoloniS@grossepointedps.org

Judge Carl Jarboe

court@grossepointepark.org

Mayor of Grosse Pointe Park, Robert Denner – dennerb@grossepointepark.org

Wayne County Prosecutor – prosecutor@waynecounty.com

State of Michigan Fraud Investigation Unit – ReportTaxFraud@michigan.gov

Grosse Pointe Park City Attorney Dennis Levasseur – DLevasseur@BODMANLAW.COM

Council Member James E. Robson

robsonj@grossepointepark.org

Mr. Robson is currently retired from his profession and has worked as a police commander and law enforcement instructor.

Council Member Lauri Read

readl@grossepointepark.org

(313)717-8777

Lauri, is an attorney in private practice and is a partner with Keller Thoma, PC in Southfield.

Council Member Vikas Relan

relanv@grossepointepark.org

Council Member Aimée Fluitt

fluitta@grossepointepark.org

Aimée spent 15 years working in national security with the FBI and NASA

Council Member Daniel C. Grano

granod@grossepointepark.org

Mr. Grano is currently an Assistant Attorney General for the State of Michigan. He is assigned to the Criminal Division and prosecutes crimes arising in the Detroit casinos, illegal gambling operations around the state, state tax crimes, and special assignments.

Council Member Michele Hodges

hodgesm@grossepointepark.org

Please hold your city officials accountable and make an example of those exposed in this website so that example can be a deterrent to future corruption. You can start by emailing the officials above.

Sincerely,

Tom Van Lokeren

tvanlok@aol.com